Ready to bring the Silvur experience to your members? Book a personalized demo now!

Lesson 3

Calculating Longevity in Your Benefits

2 min lesson

Last Updated: December 16, 2025

Your longevity can be a mix of understanding your family medical history, like what’s the average lifespan of your parents and grandparents, and whether you’re managing your health. Some questions you might ask yourself are: Do you smoke? Exercise regularly? Eat healthy? You get the idea. Although no one can predict how long they can live, you can plan your finances to last longer.

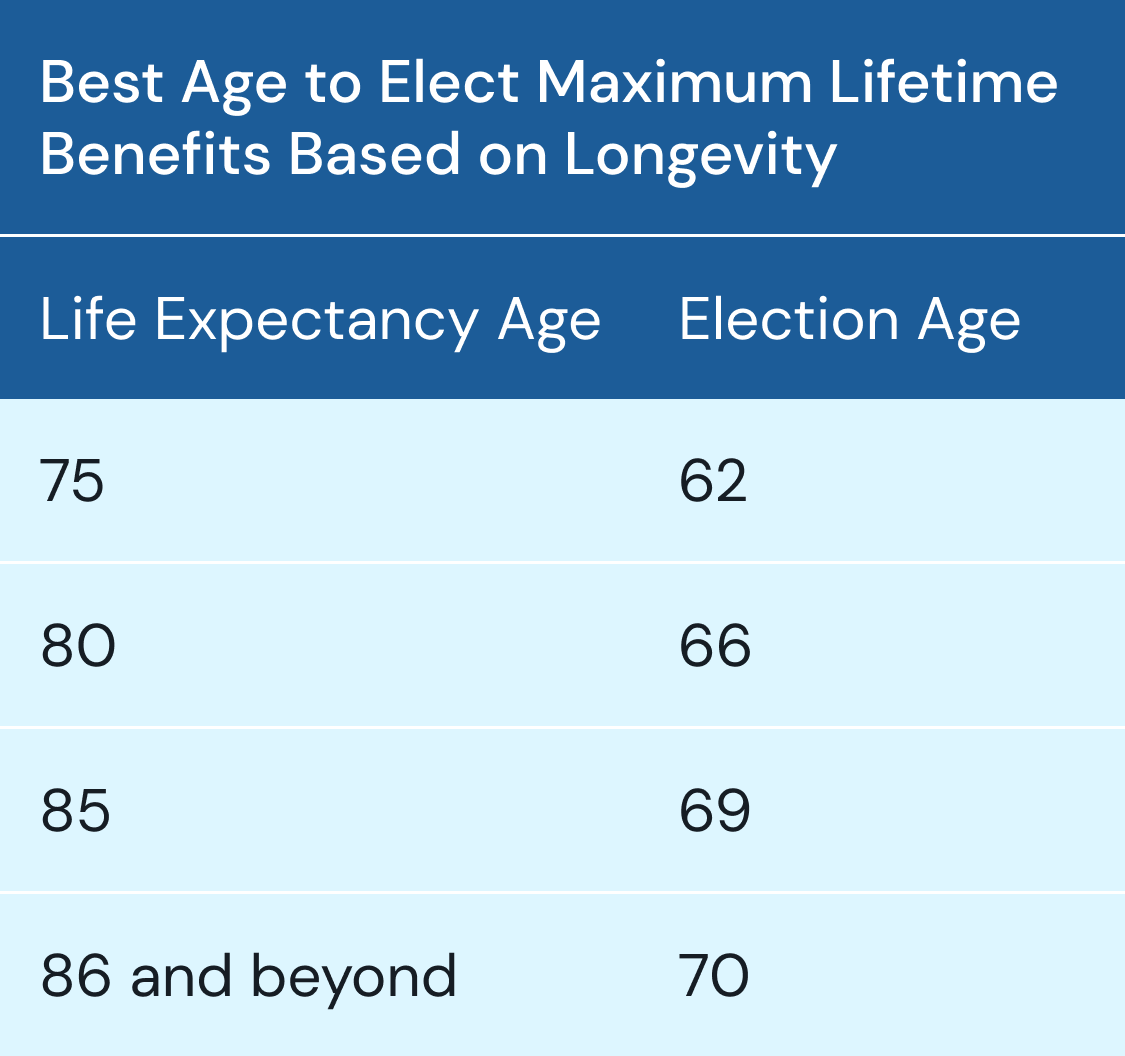

Here are our recommendations on when you should elect your benefits based on your longevity. The Social Security calculator predicts the best age to elect benefits based on your life expectancy to maximize your lifetime benefit.

Once you get a sense of your estimated longevity, enter it into the Social Security calculator. Once you do, it’ll calculate when the optimal time for you to begin claiming your Social Security benefits. If it’s looking like you might be lucky enough to live a long life, you may want to consider using a Social Security election strategy that leaves you with a financial cushion for your later years. But if you’ve been diagnosed with a chronic illness already, or you’re dealing with certain lifestyle factors that tend to put a limit on the ability to reach your 80s or 90s, it might be beneficial to elect between age 62 and your full retirement age.

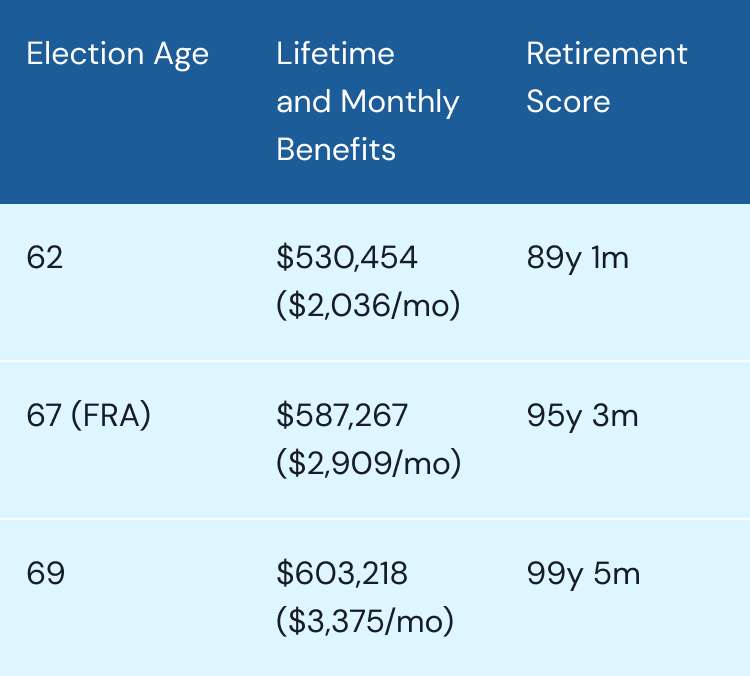

Let’s assume you’re currently 58, married, making $85,000 a year, and planning to retire at age 62. If your life expectancy is age 85, here’s the breakdown of your benefits and Retirement Score by different election ages.

In the example above, you can see that delaying your election age to 69 can add up to 10 years to your Retirement Score. Now, it’s time for you to calculate your optimal age to elect benefits based on your longevity. Go to the Social Security calculator to add your longevity to get your maximum benefit.

Bring the power of Silvur to your members