Ready to bring the Silvur experience to your members? Book a personalized demo now!

Lesson 7

Understanding Full Retirement Age

2 min lesson

Last Updated: December 16, 2025

If you’re like many workers, every day past your 62nd birthday presents a whole new temptation to apply for Social Security benefits. Yes, you do qualify, so it’s something to consider. But before pulling the trigger, we advise you to think carefully about your needs as well as those of your spouse as the future unfolds. The government doesn’t consider age 62 to be “full retirement age,” so you’ll receive a reduced benefit for the rest of your life if you claim your benefits now. In fact, if you take your benefits before full retirement age, your benefits will be reduced by a percentage for each month that you’re early.

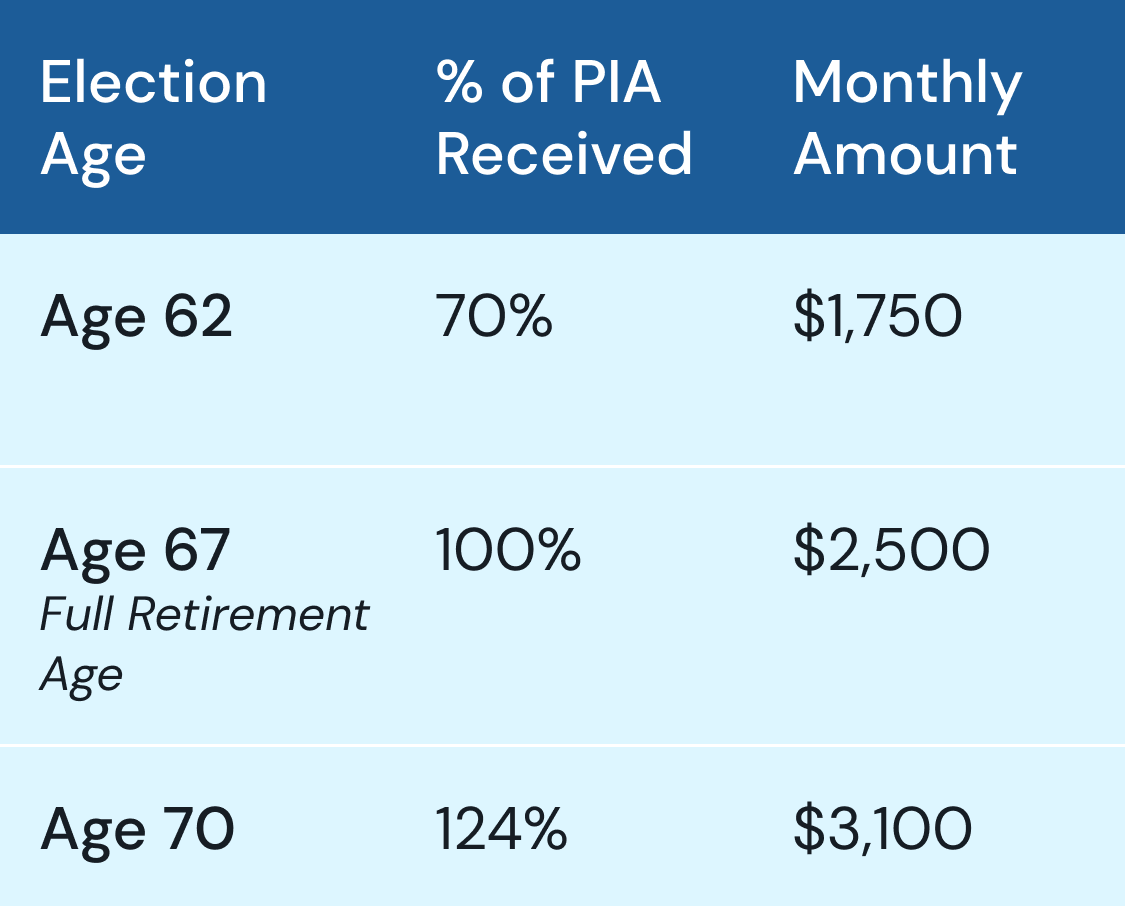

If you were born in 1960 or later, your full retirement age is 67. So taking benefits at the age of 62 shaves 60 months off of your full retirement age, substantially reducing your benefits. For example, you would receive $700 instead of $1,000 per month — a 30% reduction. Read our class “Social Security 101” to find your full retirement age. This can spark a much-needed conversation with your spouse on the best time for each of you to claim Social Security benefits.

Our Social Security calculator allows you to see exactly what type of increase or reduction you could expect based on when you elect benefits. Will you have enough? If not, know that for every year (up to age 70) that you delay taking benefits, you’ll see an 8% increase in your benefits. So waiting even a year or two means you’ll get a larger Social Security check, as shown in the example above. Note that getting a part-time job is an excellent way to bring in some much-needed income that will allow you to boost your Social Security income for the rest of your life.

Bring the power of Silvur to your members