Ready to bring the Silvur experience to your members? Book a personalized demo now!

Lesson 2

How Does Social Security Work?

9 min lesson

Last Updated: December 30, 2025

Social Security is an example of an annuity. In some ways, it can be thought of as longevity insurance. You receive income benefits for life, starting when you’re eligible and apply for it. Your benefits are based on a formula used by the Social Security Administration and rely on your employment earnings over time.

Some women worry that changing their name at marriage will impact their Social Security benefits. The good news is that there is no cost for a new Social Security card that reflects your married name. Additionally, your earnings follow your Social Security number, not your name, so changing your name won’t impact your benefits.1

Qualifying for Social Security2

You need to accumulate at least 40 Social Security credits over your lifetime in order to qualify for Social Security.

Employees receive Social Security credits as they earn money and pay Social Security and Medicare taxes. You can earn up to four credits each year. As a result, you only need to max out for 10 years in order to qualify for Social Security.

The amount of earned wages you need to receive a Social Security credit changes over time, but for 2026, you earn one Social Security credit for every $1,890 in eligible earnings. So, in order to earn four Social Security credits for 2026, you need to make at least $7,560. As a result of this threshold, it’s possible for part-time employees to earn Social Security credits and qualify for benefits later.

When Can You Elect to Receive Benefits?

It’s possible to elect Social Security benefits as early as age 62, but that’s not always the best idea. At that age, your benefits would be 30% lower than if you waited until your full retirement age (or FRA) to claim your benefits.

Wondering what your FRA would be? It’s all based on your birth year and month, but it’ll be somewhere between age 66 and 67 (see the table below). According to the Social Security Administration, once you reach your full retirement age, you’re finally entitled to 100% of your benefits, which is known as your primary insurance amount (PIA).

Deciding when to elect Social Security can significantly impact the amount of benefits you’ll receive, and waiting until age 70 will earn you the maximum monthly Social Security benefits.3

Claiming Social Security early will reduce your monthly benefit compared to waiting until full retirement age. If you start collecting at 62, your benefit will be permanently reduced—by approximately 30% less—than if you wait until full retirement age.

Then, when you hit full retirement age, you can choose to delay your benefits even further for an even better benefit: delaying benefits from your FRA up until age 70 will increase your monthly benefits by as much as 8% each year. That means you can amass a potential increase of 24% to 32%, which can be a substantial amount. However, it’s important to keep in mind that there is no additional increase in benefits past age 70. The decision to claim early comes down to choosing a lower monthly benefit over a longer period of time or a larger monthly benefit for fewer years.4

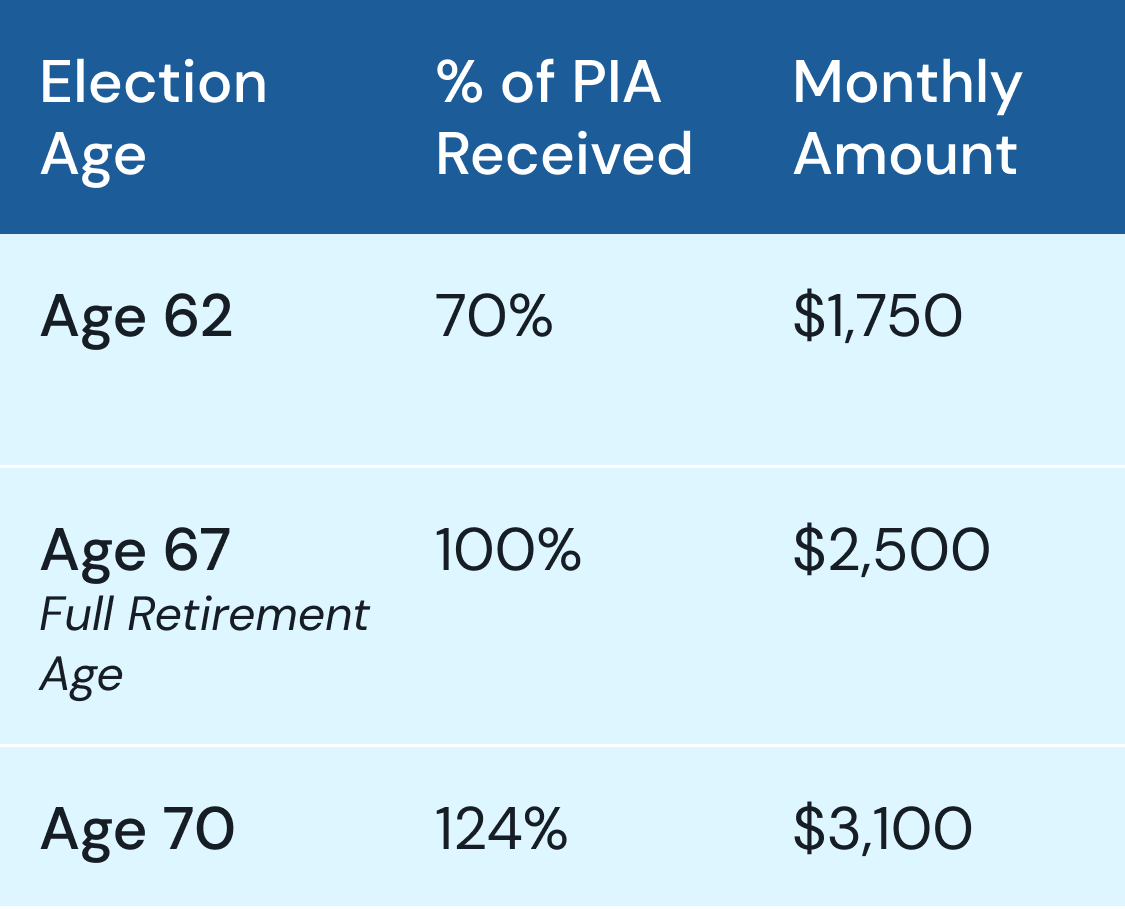

To recap, if you were to opt to receive benefits at 62, you would receive 70% of your primary insurance amount. If you wait until your full retirement age (FRA) of 67, you will receive 100% of your PIA. For every additional year up to age 70, you will receive an additional 8%, totaling up to 124% of your original PIA.4 Note that this applies to your own benefits that you’ve worked for, not spousal or survivor benefits, which come with different rules.

Let’s assume your initial PIA is $2,500 at full retirement age. Below is an example of how your benefits can increase or decrease based on election age.

How Social Security Benefits are Calculated

Your monthly Social Security benefit isn’t based on the Social Security credits you earn over time. If you accumulate more than 40 credits, you won’t see a higher benefit. Instead, your monthly Social Security payment is based on your income over time.5,6

To calculate benefits, the Social Security Administration takes your highest 35 years of earnings. However, due to inflation, your benefits are based on what is called “average indexed monthly earnings.”

Because Social Security benefits are calculated based on your income, women have greater challenges when it comes to receiving benefits. In general, they end up with 20% lower Social Security benefits than men, in part because women are more likely to take time out of the workforce, work part-time around caregiving duties and have lower-wage jobs.

Women are often expected to provide caregiving duties—at the expense of their earning power—and this may reduce Social Security benefits. Various studies indicate that:

-

A woman with one child earns, on average, 28% less over her career compared to a woman who doesn’t have children.6 This disparity is often attributed to time out of the workforce. Men do not earn less after having children.

-

Women are more likely than men to leave the workforce early to care for an aging parent, potentially resulting in about $142,000 in lost wages.7

Social Security Disability Benefits

Social Security also offers disability benefits to those who aren’t at retirement age but can no longer work.8 The credit requirement for Social Security disability benefits is lower and based on your age and how many credits you earned in the years immediately prior to the beginning of your disability:

-

Before age 24: You need to have earned six Social Security credits in the three years prior to becoming disabled.

-

Age 24 to 31: Credits needed are based on working half the time from age 21 until your disability began. For example, if you become disabled at age 29, you would need four years’ worth of employment (half of eight), or 16 credits.

-

Age 31+: You normally need to accumulate at least 20 credits in the previous 10 years before the beginning of the disability.

Once again, the highest-earning years, based on indexed earnings, are used to calculate your benefit.

What happens if you go back to work during retirement?

It’s possible to collect Social Security benefits even while you work. However, you might end up with reduced benefits, based on how much money you make during the year.

The Social Security Administration has a limit, based on whether you’re under full retirement age or whether you’ve reached full retirement age.

For 2026, if you are under your full retirement age, the annual limit to receive your full benefit payment while working is $24,480. If you make more than that amount of money, your monthly benefit will be reduced by $1 for every $2 above the threshold. On the other hand, if you will reach full retirement age in 2026 and you earn more than $65,160 prior to the month when you reach full retirement age, you will see a benefit reduction of $1 for every $3 over the limit.

The good news is that once you reach full retirement age, you can receive your Social Security benefits no matter how much you make.

When considering how long to work and when to start taking benefits, think about the potential for reductions in your benefits. While you work, you will continue to pay Social Security taxes, so there’s the potential to see an increase in monthly benefits down the road, based on how much you’re paying in—even if you are receiving Social Security benefits.

SOURCES

- “Social Security for Women.” Social Security Administration. https://www.ssa.gov/people/women/. Accessed 16 December 2025.

- “Quarter of Coverage.” Social Security Administration. https://www.ssa.gov/oact/cola/QC.html Accessed 16 December 2025

- “Delayed Retirement Credits.” SSA, Social Security Administration, https://www.ssa.gov/benefits/retirement/planner/delayret.html. Accessed 16 December 2025.

- “Retirement Benefits.” SSA, Social Security Administration, https://www.ssa.gov/benefits/retirement/planner/1960.html. Accessed 16 December 2025.

- “Social Security Benefit Amounts.” Social Security Administration. https://www.ssa.gov/oact/cola/Benefits.html. Accessed 16 December 2025.

- “Benefit Calculation Examples for Workers Retiring in 2026.” Social Security Administration. https://www.ssa.gov/oact/ProgData/retirebenefit1.html. Accessed 16 December 2025.

- “How Much Does Motherhood Cost Women in Social Security Benefits?” SSRN.com. 9 October 2017. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3048891. Accessed 16 December 2025.

- “Social Security Credits.” Social Security Administration. https://www.ssa.gov/benefits/retirement/planner/credits.html. Accessed 16 December 2025.

Bring the power of Silvur to your members